Click the icon to add a specified price to your Dashboard list. This makes it easy to keep track on the prices that matter most to you.

This week, LLDPE prices gained in parts of Asia.

An industry source in Asia on condition of anonymity informed a Polymerupdate team member, “Prices strengthened as suppliers from the Middle East made firmer April offer announcements; however, buyers were hesitant to commit to purchases due to low demand from end users.”

The source added, "Global oil prices experienced a decline as markets weighed the potential impact of a dampened demand outlook stemming from U.S. tariff policies, implying a shift in focus from the effect of imposition of sanctions on oil-producing nations."

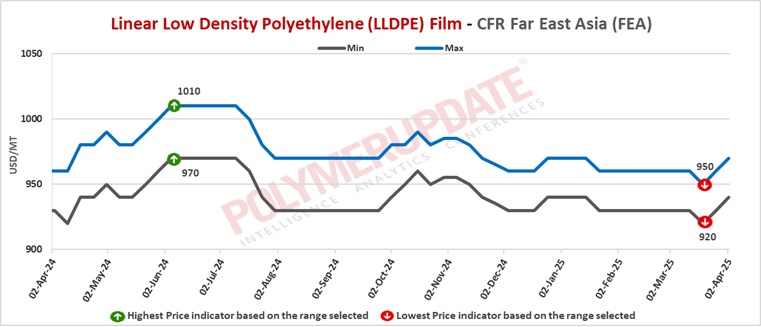

In Far East Asia, LLDPE prices were assessed at USD 940-970/mt CFR levels, an increase of USD (+10/mt) from the previous week.

In China, Middle Eastern producers have offered their LLDPE film grades in the range of USD 940-970/mt levels, for shipment in April 2025.

In China, polyethylene (PE) import prices continue to face pressure as a result of low purchasing interest and declining domestic market prices. Deteriorating import price netbacks have prompted overseas suppliers to reroute their shipments to markets experiencing tighter supply. Although increasing maintenance costs may offer temporary price support, downstream buyers are restocking their inventories in anticipation of the holiday season, albeit with a cautious outlook. Improvements in supply and demand remain minimal. Meanwhile, U.S. dollar prices experienced a slight uptick compared to the previous week, supported by moderate trading activity and a minor appreciation of the RMB.

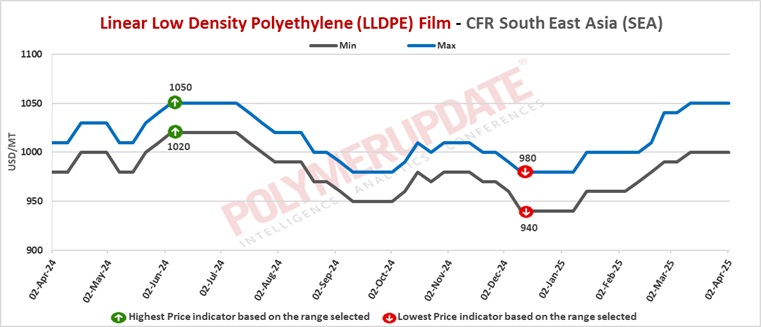

In Southeast Asia, LLDPE prices were assessed at USD 1000-1050/mt CFR levels, unchanged week on week.

In Southeast Asia, the PE market is anticipated to experience a slowdown in early April, primarily due to holiday-related disruptions such as Eid al-Fitr in Indonesia and Malaysia, as well as Songkran in Thailand. There has been a decline in purchasing sentiment, as many converters have already acquired adequate supplies and are hesitant to increase their inventories. In Vietnam, market activity has diminished; however, there is some price support from a major supplier in the Middle East, although transactions remain unconfirmed and limited in scope.

The lower segment of the price spectrum continues to be pressured by an oversupply situation, which includes competitively priced HDPE from the U.S. being resold by traders and end-users. Looking forward, demand is likely to stay subdued in the first half of April, with the possibility of a rebound later in the month, contingent upon supply conditions and overall economic factors.

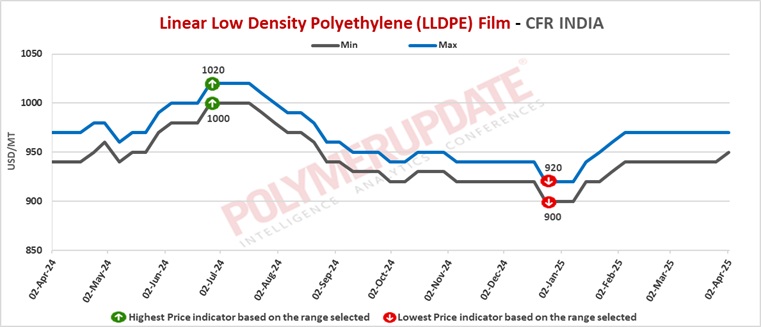

In India, LLDPE prices were assessed at the USD 950-970/mt CFR levels, an increase of USD (+10/NC/mt) from last week.

In India, Middle Eastern producers have offered their LLDPE film grades in the range of USD 950-970/mt levels, for shipment in April 2025.

A domestic industry source informed a Polymerupdate team member, “Reliance Industries Limited (RIL) announced price revision in PE, with effect from April 1, 2025. LLDPE Roto molding grade prices have been decreased by Rs.3/kg basic while High Flow grade prices have been lowered by Re.1/kg basic. Meanwhile, all other LLDPE grade prices have been rolled over.”

In India, polyethylene (PE) market prices are likely to remain stable to firm in the short term. A reduction in domestic supply, attributed to maintenance activities at production facilities, is anticipated to bolster prices. Nevertheless, demand is expected to stay weak, characterized by minimal restocking efforts and a lack of significant incentives for heightened consumption. Meanwhile, the overall market sentiment will be influenced by new offers in April and wider economic conditions.

In Pakistan, LLDPE prices were assessed at the USD 980-990/mt CFR levels, a rise of USD (+10/NC/mt) from the previous week.

In Pakistan, Middle Eastern producers have offered their LLDPE film grade in the range of USD 980-990/mt levels for shipment in April 2025.

In Pakistan, PE market conditions have been characterized by a period of minimal purchasing activity, primarily influenced by several external factors. The Islamic holy month of Ramadan contributed to a decrease in market activities as consumer spending typically slows during this period. Additionally, political unrest in the country has the potential to create uncertainties that can discourage investment and adversely impact buying decisions within the polymer sector.

Currency fluctuations have further exacerbated the situation, impacting the cost structures and pricing strategies for polymer products. This volatility has created an atmosphere of caution among buyers and sellers, leading to a predominantly bearish sentiment in the market. As a result, participants in the polymer market are more hesitant to engage in transactions, contributing to the reduced activity overall.

In Sri Lanka, LLDPE prices were assessed at the USD 1000-1020/mt levels, a week on week gain of USD (+10/NC/mt).

In Sri Lanka, Middle Eastern producers have offered their LLDPE film grade in the range of USD 1000-1020/mt levels for shipment in April 2025.

In Sri Lanka, the polyethylene market in Sri Lanka remained stable, with limited spot offers circulating in the region. The lack of significant fluctuations in price is attributed to a steady regional demand; however, restocking activities have been minimal as distributors and manufacturers are likely awaiting the upcoming New Year celebrations in the country.

This anticipation has led to cautious purchasing behaviour, with entities preferring to hold off on bulk restocking until after the festivities. As a result, the overall market dynamics for polyethylene in Sri Lanka reflect a period of consolidation, with prices staying firm amidst a backdrop of restrained activity and demand. In Bangladesh, LLDPE prices were assessed at the USD 1020-1050/mt CFR levels, rolled over from last week.

In Bangladesh, LLDPE prices were assessed at the USD 1020-1050/mt CFR levels, rolled over from last week.

In Bangladesh, PE prices remained stable amid a notable decline in trading activity as the Eid festivities approached. The market typically experiences a slowdown during this time as businesses and consumers prepare for the celebrations.

Furthermore, a major Saudi producer entered the market with a preliminary pricing offer, which, however, was ultimately rejected. The rejection stemmed from potential buyers viewing the pricing as excessively high, highlighting a disparity between the producer's expectations and the local market's readiness to pay. In summary, the interplay of the holiday season and elevated pricing proposals led to a more restrained trading atmosphere in the polyethylene market.

Feedstock ethylene prices on Tuesday were assessed at the USD 850-860/mt CFR North East Asia levels while CFR South East Asia ethylene prices were assessed at the USD 915-925/mt levels, both quoting flat week on week.

In plant news, GAIL (India) Limited is heard to have taken off stream its Linear low density polyethylene/High density polyethylene (LLDPE/HDPE) swing unit for a maintenance turnaround. The unit is likely to remain shut till the last week of April 2025. Located in Pata, Uttar Pradesh, India, the LLDPE/HDPE swing unit has a production capacity of 400,000 mt/year.

In other plant news, Pengerang Refining and Petrochemical (PRefChem) has prolonged the shutdown of its polyethylene (PE) units to mid-May 2025. The units were taken off stream in early February 2025 for maintenance with operations scheduled to restart in early April 2025. Located in Pengerang, Malaysia, the PE units have an HDPE production capacity of 400,000 mt/year and LLDPE production capacity of 350,000 mt/year.