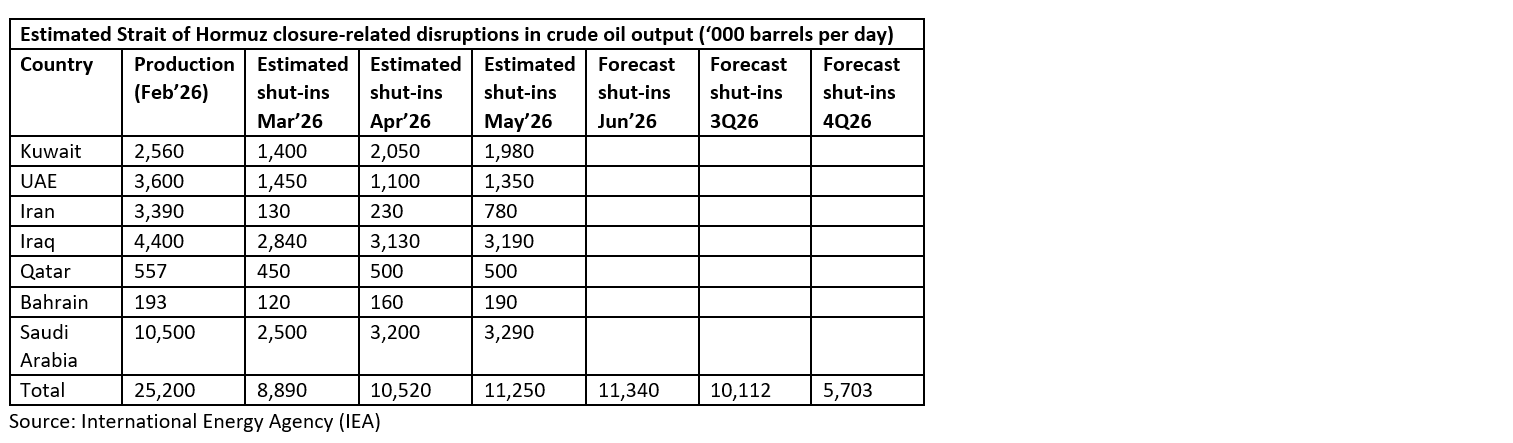

Around 50 percent of the disrupted crude oil output in the Middle East is likely to return only after the end of calendar year 2026 due to the extensive reconstruction and redevelopment required to fully restore production activities, the International Energy Agency (IEA) said in its latest study released recently. This implies that only half of the shut-in capacity damaged during the past four months of the U.S.-Israel war with Iran and Tehran's subsequent retaliatory attacks across the Gulf region is expected to resume operations over the next six months, even if the ongoing ceasefire holds.

The IEA estimates that disrupted crude oil production in the Middle East rose to 11.25 million barrels per day (bpd) in May and further increased to 11.34 million bpd in June. The agency expects shut-in production capacity to remain elevated at around 10.11 million bpd during the July-September quarter, primarily due to storage facilities—particularly in Iran—reaching their maximum capacity, forcing producers to shut in additional volumes as the closure of the Strait of Hormuz persisted. Although the Strait of Hormuz, the strategic chokepoint that handles around one-fifth of global seaborne crude oil trade, has since reopened, Gulf producers are expected to wait for a more durable resolution to the Middle East conflict before restoring production to full capacity.

According to IEA, approximately 5.7 million barrels per day (bpd) of crude oil production shut in due to the conflict is expected to remain offline through the end of 2026. This represents nearly 50 percent of the total disrupted output, indicating that a significant portion of the region's lost production capacity will not return in the near term. While a gradual recovery in output is anticipated as security conditions improve and damaged infrastructure is restored, the pace of normalization is likely to remain slow, leaving global oil markets vulnerable to supply tightness and renewed geopolitical risks.

Pre-war forecasts

Pre-war forecastsBefore the outbreak of the conflict, the global oil market was well positioned to absorb a temporary disruption in supplies, supported by several months of oversupply and substantial inventory builds across both onshore and floating storage facilities. These ample stockpiles initially acted as a buffer against supply shocks, helping stabilize markets despite interruptions to crude flows from the Middle East. However, as the conflict dragged on and supply disruptions persisted, global oil inventories were increasingly drawn down to meet demand, gradually eroding this cushion.

Assuming the Strait of Hormuz reopens and oil trade flows gradually resume, analysts expect OECD commercial liquid fuel inventories to decline sharply to just under 2.3 billion barrels by December 2026. Such a level would be the lowest since comparable records began in 2003 and would stand well below the 2021–2025 five-year average of approximately 2.8 billion barrels. The projected decline underscores the growing strain on global oil balances and suggests that, even with the gradual restoration of Middle East exports, inventories are likely to remain historically tight, leaving crude markets increasingly vulnerable to renewed supply disruptions and geopolitical shocks.

Middle East war and its impactThe U.S.-Israel conflict with Iran started on February 28, followed by Tehran's retaliatory missile strikes on critical energy infrastructure across the Middle East, has dealt a severe blow to regional oil supplies and heightened concerns over global energy security. Several major oil fields, production facilities and refineries across the region sustained varying degrees of damage, forcing operators to either partially curtail or completely suspend production. The disruption has removed millions of barrels per day of crude oil and refined products from the market, tightening global supplies and driving renewed volatility in energy prices.

Beyond the immediate loss of production, the attacks have exposed the vulnerability of the Middle East's energy infrastructure, which accounts for a significant share of the world's crude oil exports. Repairing damaged facilities and restoring full production capacity is expected to take months in some cases, prolonging supply constraints even if hostilities ease. The conflict has also disrupted regional logistics, delayed crude exports, and increased shipping and insurance costs, reinforcing concerns that geopolitical tensions in West Asia could continue to weigh on global oil markets well into 2026.

Consumption to declineThe IEA expects that high fuel prices, reduced fuel availability and government-led demand restraint measures have weighed on global oil consumption in recent months. The slowdown in demand has helped limit draws on global oil inventories despite significant supply disruptions. The agency has revised down its global oil demand growth outlook, citing government initiatives to curb fuel consumption, widespread fuel shortages and reduced exports of refined petroleum products. Most of the decline in demand has been concentrated in Asia, which relies heavily on crude oil supplies from the Middle East.

Although timely demand data remain limited, particularly for Asian countries most affected by the closure of the Strait of Hormuz, available indicators suggest that oil consumption has fallen by more than previously estimated. As a result, the IEA now forecasts global oil demand will decline by an average of 1.1 million barrels per day (bpd) in 2026, compared with its previous forecast last month for growth of 0.2 million bpd and its February projection for growth of 1.2 million bpd. The agency expects demand to rebound in 2027 as oil prices ease and supply flows gradually normalize later in 2026, with global oil consumption projected to increase by 2.5 million bpd to 105.3 million bpd.

DILIP KUMAR JHA

Editor

dilip.jha@polymerupdate.com