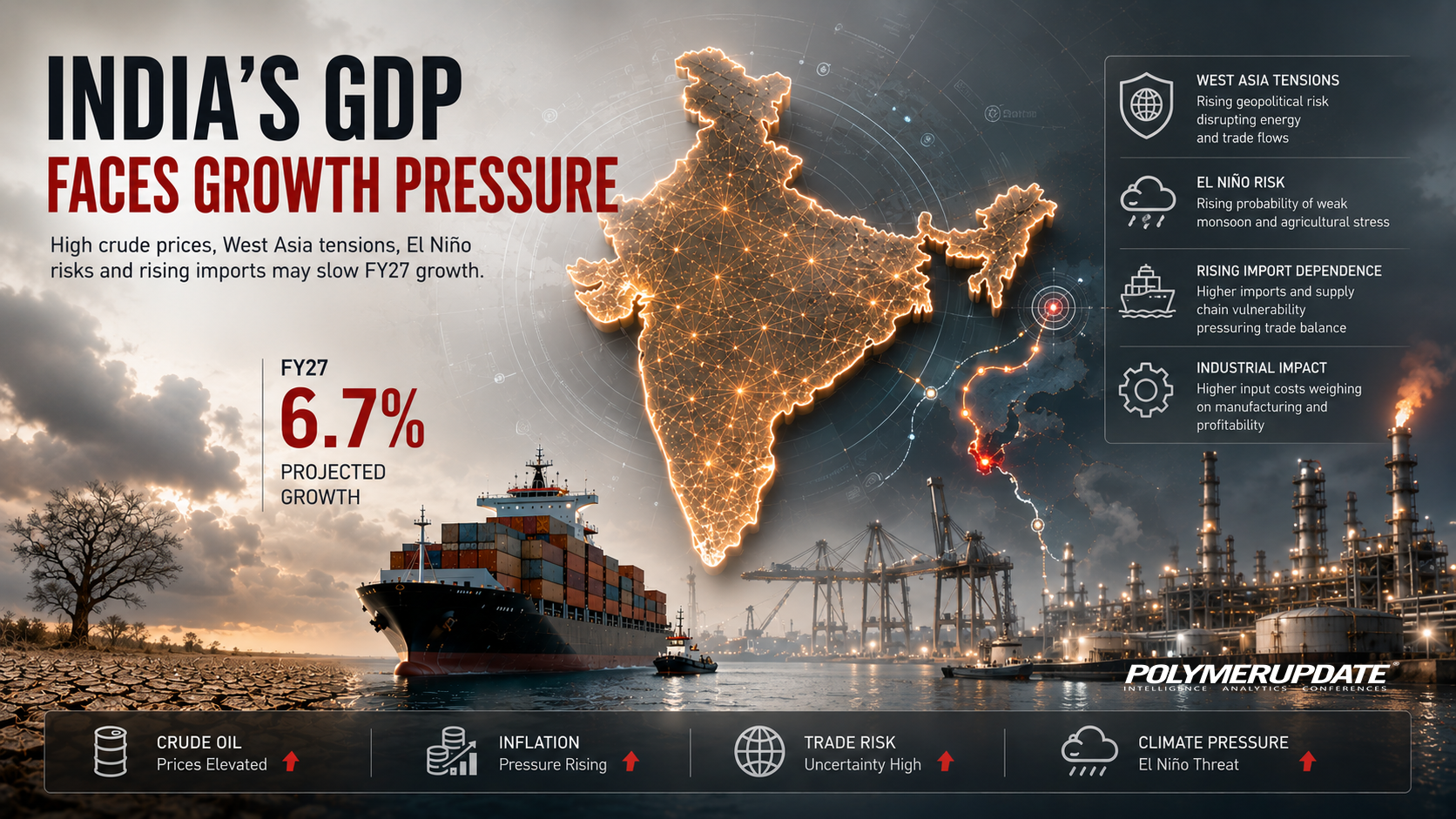

Elevated crude oil prices arising from supply disruptions caused by the West Asia crisis, coupled with the likely occurrence of El Niño, are expected to slow India’s economic growth to 6.7 percent in the financial year (FY) 2026-27, according to the latest study released today by India Ratings and Research. The study, conducted for the first time using 2022-23 as the base year, projects India’s gross domestic product (GDP) growth for FY2026-27 substantially lower than the 7.6 percent recorded in the previous year.

The projection is broadly in line with the World Bank’s estimate of 6.6 percent GDP growth for FY2026-27 and the International Monetary Fund’s (IMF) forecast of 6.5 percent. Both international institutions released their projections in April. However, Citi and Bank of America Merrill Lynch (BofA ML), in the pre-Middle East war period, had projected India’s GDP growth at 7.4 percent and 7.1 percent, respectively. Meanwhile, the Reserve Bank of India (RBI), following the Monetary Policy Committee meeting held in April, estimated India’s GDP growth at 7.9 percent for FY2026-27, compared with 7.6 percent projected for the previous year.

The study found that higher fuel and food prices resulting from uncertainty surrounding the West Asia conflict, along with the likely impact of an evolving El Niño on agriculture from mid-2026, could weigh on GDP growth in FY27. In its baseline forecast, the agency has assumed crude oil prices at US$ 95 a barrel. If the West Asia conflict is resolved quickly and oil prices average below US$ 95 a barrel in FY2026-27, GDP growth could improve. A weaker-than-expected El Niño and stronger capital inflows could also support growth beyond the current estimate.

Megha Arora, Economist and Director, Public Finance at India Ratings, said, “Major headwinds include geopolitical developments, particularly the West Asia conflict, high headline inflation, a depreciating currency due to weak capital inflows, weaker-than-expected capital expenditure, especially by the government to contain fiscal risks, weak global trade growth, the high base effect from strong FY2025-26 growth, subdued industrial production as measured by the Index of Industrial Production (IIP), and notably, the likely El Niño weather pattern from mid-2026. A US$ 10 a barrel increase in crude oil prices could reduce GDP growth by 44 basis points (bps), while a 10 percent reduction in capex could lower GDP growth to 6 percent.”

Dependence on imports

Dependence on importsIndia’s crude oil demand is steadily rising and is now estimated at around 5.5 million barrels per day (bpd), driven by strong economic growth, rapid urbanisation, and rising fuel consumption across the transport, manufacturing, and petrochemical sectors. As the world’s third-largest oil consumer, India continues to witness higher energy needs amid expanding industrial activity, increasing vehicle ownership, and sustained infrastructure development. Demand for petrol, diesel, and aviation turbine fuel has remained robust, reflecting resilient domestic consumption despite global economic uncertainties and periodic volatility in crude prices.

At the same time, India remains heavily dependent on overseas crude supplies, with nearly 85 percent of its oil requirement met through imports. This high import dependence leaves the country vulnerable to fluctuations in global crude prices, geopolitical tensions, and supply disruptions, particularly in key producing regions such as the Middle East. Any disruption in shipping routes such as the Strait of Hormuz, or sharp movements in international benchmark prices, directly impacts India’s import bill, trade deficit, and inflation outlook. As a result, energy security continues to remain a major policy priority for the government.

To reduce the long-term risks associated with rising import dependence, India has been focusing on diversifying its crude sourcing basket, expanding strategic petroleum reserves, and accelerating investments in renewable energy and alternative fuels. Policymakers are also encouraging ethanol blending, electric mobility, and domestic exploration to gradually reduce reliance on imported crude oil. However, given the country’s fast-growing economy and rising energy consumption, crude oil is expected to remain a critical component of India’s energy mix for the foreseeable future, keeping import dependence structurally high in the coming years.

Economy’s vulnerability to monsoonIndia’s economic growth remains vulnerable to high crude oil prices and deficient rainfall. However, vulnerability arising from rainfall has declined over the past decades due to: (i) higher irrigation coverage, with irrigation intensity — defined as gross irrigated area as a percentage of gross cropped area — rising to 55.7 percent in FY23 from 41.1 percent in FY01; (ii) improvements in agricultural extension facilities; (iii) a higher share of allied agricultural activities such as livestock and forestry; and (iv) the growing contribution of the services sector to gross value added (GVA).

If the spatial distribution of rainfall during the June-September period remains close to the normal pattern, the risk to agricultural GVA could be lower. However, the combined impact of high crude oil prices and below-normal rainfall on GDP growth remains significant.

The study further found that India’s high dependence on crude oil imports constrains economic growth during volatile periods such as the current one, when supply disruptions affect manufacturing and allied activities. Under various FY27 crude oil price assumptions, the agency estimates that a US$ 10 a barrel increase in crude oil prices could reduce GDP growth by 44 basis points (bps). With one-third of the higher crude prices passed on to consumers, retail inflation, measured by the Consumer Price Index (CPI), could rise by 93 bps, while the current account deficit (CAD)-to-GDP ratio could widen by 43 bps.

Government measuresThe West Asia crisis has the potential to escalate into a balance-of-payments crisis, driven by supply chain bottlenecks, elevated commodity prices, and supply shortages. The agency expects the government to counter any adverse impact arising from the West Asia crisis through credit measures, such as credit guarantees, rather than direct spending, thereby reducing pressure on the current fiscal position.

The Indian government has projected a fiscal deficit of 4.3 percent for FY27, although achieving this target may prove challenging due to higher fuel and fertiliser subsidies, reduced excise duties on petrol and diesel to cushion the impact of rising energy prices, and likely monetary support measures to counter the effects of El Niño. The fiscal stabilisation fund of INR 1 trillion, created in FY26, is also expected to help limit the fiscal deficit and borrowing requirements in FY27.

To protect consumers, the government has reduced excise duties on petrol and diesel while increasing prices for certain categories of fuel. Retail prices of premium petrol and diesel, liquefied petroleum gas (LPG), aviation turbine fuel (ATF), and industrial diesel were increased during March-April 2026. Retail prices of petrol and diesel were further raised by INR 3 per litre each, while compressed natural gas (CNG) prices were increased by INR 2 per kg on May 15, 2026. Earlier, in March 2026, the government had reduced excise duties on petrol and diesel by INR 10 per litre.

DILIP KUMAR JHA

Editor

dilip.jha@polymerupdate.com