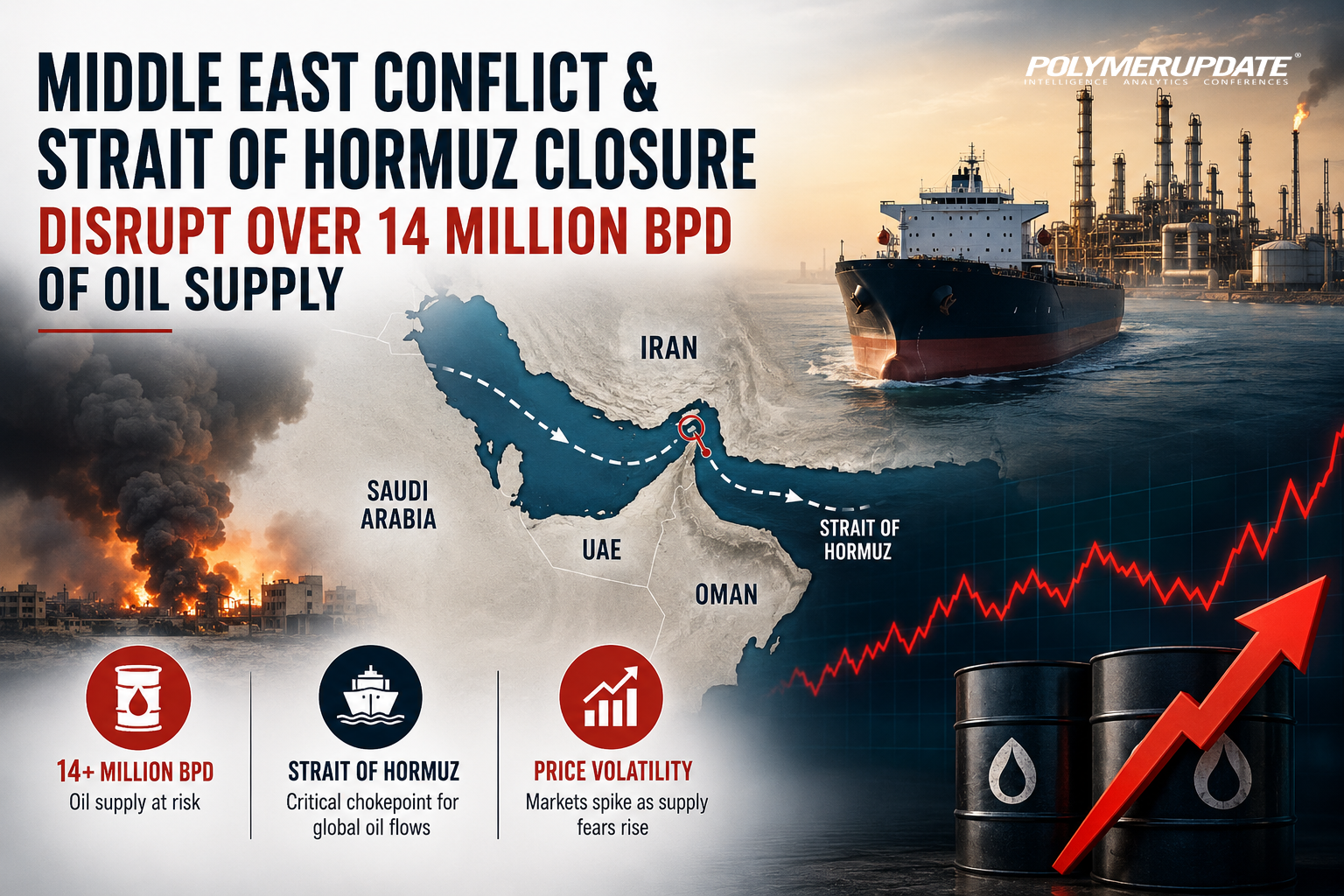

Gulf oil producers have lost more than 14 million barrels per day (bpd) of crude supply, with cumulative disruptions approaching 1 billion barrels, following the closure of the Strait of Hormuz and retaliatory Iranian drone and missile attacks after the United States and Israel jointly struck Tehran on February 28, 2026, the International Energy Agency (IEA) said in its latest report. The Strait of Hormuz, a critical maritime chokepoint that handles nearly one-fifth of global oil shipments, has become the focal point of the supply crisis. According to the IEA, the conflict in the Middle East has triggered an unprecedented supply shock, driving up global energy prices, fuelling inflationary pressures and weakening global economic growth prospects.

Benchmark crude oil prices have witnessed extreme volatility amid conflicting signals over whether the United States and Iran could reach an agreement to end the conflict and reopen the Strait of Hormuz. North Sea Dated crude plunged from a high of US$ 144 a barrel to below US$ 100 a barrel before rebounding to around US$ 110 a barrel as negotiations remained deadlocked. Both Washington and Tehran continued to harden their rhetoric, warning of severe consequences if hostilities escalate further, keeping global energy and financial markets on edge.

The sharp decline in Gulf oil supplies prompted swift responses from both producing and consuming nations. Countries such as India called for measures to curb fuel consumption, while several governments encouraged work-from-home arrangements for public sector employees to reduce energy demand. Despite the disruption, the current supply-demand gap remains relatively narrower as the global oil market had already been in surplus before the crisis began, while both producers and consumers have adjusted rapidly to changing market conditions. However, more than ten weeks after the conflict erupted, mounting supply losses linked to the Strait of Hormuz continue to deplete global oil inventories at a record pace.

Supply-side response

Supply-side responseOn the supply side, Saudi Arabia and the United Arab Emirates (UAE) have managed to redirect part of their crude exports to terminals located outside the Strait of Hormuz, helping to ease some of the disruption caused by the ongoing conflict. At the same time, commercial inventories and government strategic petroleum reserves in major consuming nations are being released into the market to offset part of the supply losses. According to the International Energy Agency (IEA), global oil inventories, including crude stored on water, declined by nearly 250 million barrels during March and April, equivalent to around 4 million barrels per day (bpd). Producers outside the Middle East also responded swiftly by increasing output and pushing exports to record levels in an attempt to stabilize global supplies.

The IEA said supply growth expectations from the Americas for 2026 have been revised upward by more than 0.6 million bpd since the beginning of the year, taking total projected growth to an average of 1.5 million bpd. Crude exports from the Atlantic Basin — now increasingly directed towards severely affected East of Suez markets — have surged by around 3.5 million bpd since February, driven by higher shipments from the United States, Brazil, Canada, Kazakhstan and Venezuela. Russia’s crude exports have also increased after repeated attacks on domestic refineries reduced local consumption, leading to higher overseas shipments. In addition, the United States temporarily eased sanctions on Russian oil cargoes already at sea, further supporting global supplies amid the ongoing crisis.

Demand-side initiativesOn the demand side, refiners have reduced processing runs and sharply scaled back crude oil imports. Chinese seaborne crude imports fell by a massive 3.6 million bpd between February and April, according to Kpler. Major reductions in imports were also recorded in Japan (-1.9 million bpd), South Korea (-1 million bpd) and India (-0.76 million bpd). However, while the slowdown in global refinery activity — by around 5 million bpd year-on-year in April — has temporarily eased tensions in the crude market, tightness is rapidly spreading to product markets. End users are also cutting back on fuel consumption.

As a result, global oil demand is now expected to contract by 2.4 million bpd year-on-year during the April-June quarter of 2026 and decline by 420,000 bpd for the year as a whole, which is 1.3 million bpd weaker than the pre-conflict forecast. For now, the steepest demand losses are being seen in the petrochemical sector, where feedstock availability is becoming increasingly constrained. Aviation activity is also running well below normal levels, helping to ease some pressure on jet fuel prices, which nearly tripled after Middle Eastern exports were disrupted. Higher prices, a worsening economic environment and demand-saving measures are expected to weigh further on global oil consumption.

OutlookWhile global oil demand could return to growth towards the end of the year if a peace agreement is reached and crude flows through the Strait of Hormuz gradually resume from the July-September quarter of 2026, as assumed in the report, supply recovery is expected to remain relatively slow. Consequently, the global oil market is likely to stay in deficit until the final quarter of the year. With worldwide oil inventories already declining at a record pace, markets are expected to remain highly volatile ahead of the peak summer demand season.

DILIP KUMAR JHA

Editor

dilip.jha@polymerupdate.com