Click the icon to add a specified price to your Dashboard list. This makes it easy to keep track on the prices that matter most to you.

Renewed tensions in the Persian Gulf are forcing a fundamental repricing of seaborne crude and petrochemical feedstocks. For energy markets long accustomed to treating Hormuz risk as a theoretical footnote, the calculus has decisively shifted.

|

SETTING THE SCENE

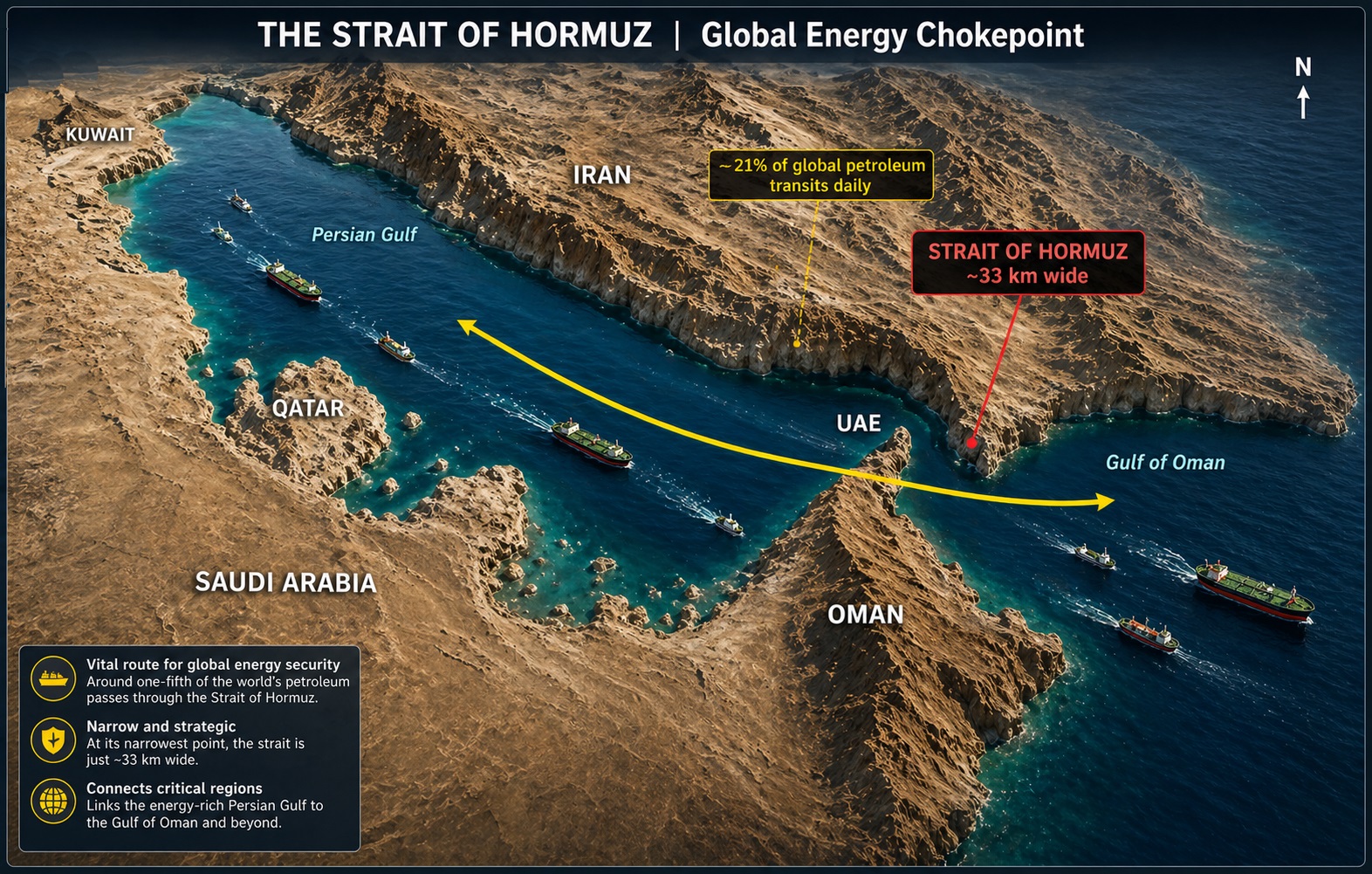

The Strait of Hormuz — a navigable channel barely 33 kilometres wide at its narrowest point — is the single most consequential maritime corridor in the global energy system. Under normal conditions, approximately one-fifth of the world’s total petroleum liquids pass through it daily, alongside a substantial share of Qatar’s liquefied natural gas exports. There is no meaningful bypass. The alternative routes — the Abqaiq-Yanbu pipeline and the Abu Dhabi Crude Oil Pipeline — carry combined spare capacity well below the volumes that transit the Strait.

Figure 1: The Strait of Hormuz — the world’s most critical energy chokepoint, with approximately 21% of global petroleum liquids transiting daily.

Against this structural reality, a renewed deterioration in Gulf security conditions is no longer a tail risk to be modelled and set aside. It is an active variable in crude pricing, shipping economics, and downstream feedstock strategy. The question facing market participants is not whether a Hormuz premium exists — it plainly does — but how durable it is, and how far it will propagate through the petrochemical value chain.

The Strait’s importance to global energy security is structural, not cyclical. Any material disruption would cascade through oil, LNG, and petrochemical markets simultaneously — a scenario for which no adequate contingency infrastructure exists.”

CRUDE BENCHMARKS: A MARKET DIVIDED BY GEOGRAPHY

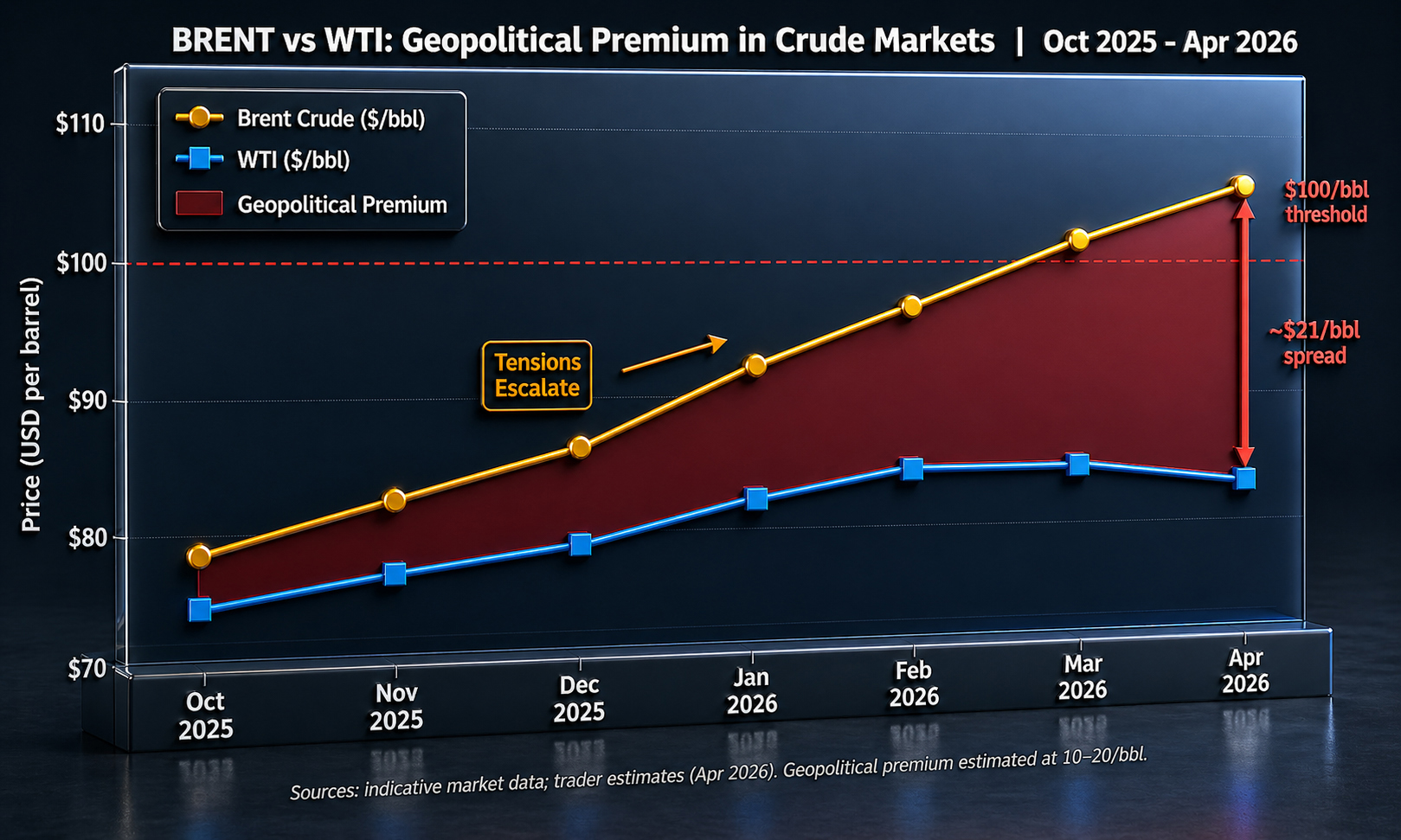

The most immediate market signal is the divergence between Brent crude and West Texas Intermediate (WTI). Brent, as the global benchmark for seaborne oil, is acutely sensitive to supply disruption risk in the Gulf. WTI, priced at Cushing, Oklahoma, reflects predominantly domestic US supply-demand dynamics and is structurally insulated from direct Hormuz exposure.

With Brent holding firmly above the $100 per barrel threshold — underpinned by both physical risk and the insurance premium now embedded in tanker freight — and WTI softening on comfortable domestic inventory levels, the resulting spread is less an arbitrage signal than a geographic verdict. Seaborne barrels are being repriced for uncertainty; landlocked barrels are not.

Figure 2: Brent vs WTI price divergence (Oct 2025–Apr 2026), illustrating the growing geopolitical risk premium in seaborne crude.

Traders across the Gulf and Singapore are currently estimating an embedded geopolitical risk premium of between $10 and $20 per barrel in Brent — a range that accounts for both direct supply disruption probability and the sharply elevated cost of war-risk insurance on tanker voyages through the region. This is not speculative froth; it is the market doing precisely what markets are designed to do: pricing known unknowns.

“The market is not pricing a closure — it is pricing the permanent possibility of one. That distinction matters enormously for how you structure your book. A closure is a crisis you hedge for once. A persistent threat is a cost of doing business you have to build into every cargo, every freight rate, every refining margin.”

— Senior crude trader, international energy trading house (Gulf region)

Brent: Firm above $100/bbl, reflecting seaborne supply vulnerability and war-risk insurance costs.

WTI: Softer, insulated by domestic inventory build and no direct Hormuz exposure.

Spread: Estimated geopolitical premium embedded in Brent: $10–$20/bbl, per trader estimates.

DIPLOMACY: ACTIVE CHANNELS, NO RESOLUTION IN SIGHT

Washington has publicly maintained a posture of guarded engagement. Statements from US administration officials have pointed to open channels with Tehran, and intermediary routes — including via Pakistan — have been floated as potential conduits for indirect dialogue. The public messaging is calibrated to signal neither confrontation nor capitulation.

Tehran’s posture, as articulated through its Foreign Ministry, tells a different story. Iranian officials have consistently emphasised sovereignty over its nuclear programme and made clear that substantive negotiations would require significant preconditions. The gap between what Washington is willing to offer and what Tehran is prepared to accept remains wide, and the choreography of engagement — however sophisticated — should not be mistaken for convergence.

For energy markets, the operative variable is not diplomatic activity but diplomatic outcome. Talks may be ongoing, but resolution — the kind that materially reduces Hormuz transit risk — is not imminent. Markets pricing a geopolitical premium are doing so rationally.

THE OPERATIONAL DIMENSION: NAVAL POSTURE AND TRANSIT RISK

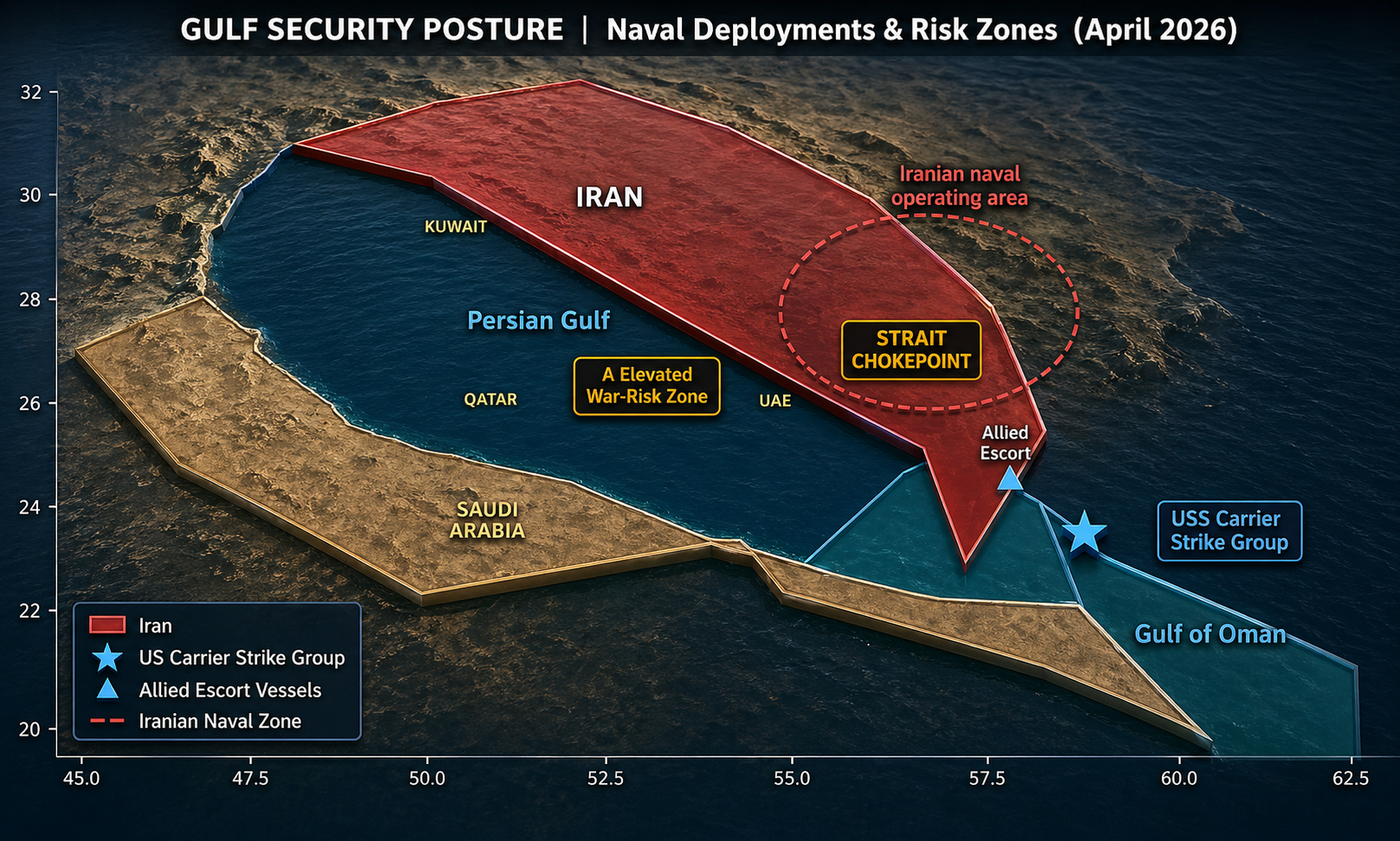

Beyond diplomatic signalling, the operational environment in the Gulf has tightened measurably. US naval presence in the region has been reinforced, with carrier strike group deployments serving both as deterrent signal and as evidence of the administration’s assessment of escalation risk. Allied navies — including those of the UK and France — maintain coordinated escort and surveillance operations.

Figure 3: Gulf security posture as of April 2026, showing US carrier strike group deployment, allied escort positions, and elevated war-risk zones around the Strait.

The practical consequence for energy flows is felt most directly in maritime insurance markets. War-risk premiums for tankers transiting the Strait have risen sharply, adding directly to the cost of Gulf crude delivered to Asia and Europe. These costs are not absorbed by shipowners alone; they are priced into cargo rates and ultimately into the landed cost of crude — a mechanism that transmits geopolitical risk into refinery economics with a lag of days rather than weeks.

It is important to note that a full closure of the Strait — sometimes invoked as a scenario in market commentary — would represent an event of extraordinary severity. Emergency Strategic Petroleum Reserve releases from the US, China, and OECD member states would be triggered rapidly. A naval coalition response would follow within days. Price spikes would be severe and immediate. The current market configuration does not price a closure; it prices an elevated and sustained risk of disruption. That is a meaningful, but importantly different, scenario.

PETROCHEMICALS: FEEDSTOCK DIVERGENCE AND THE COMPETITIVENESS SHIFT

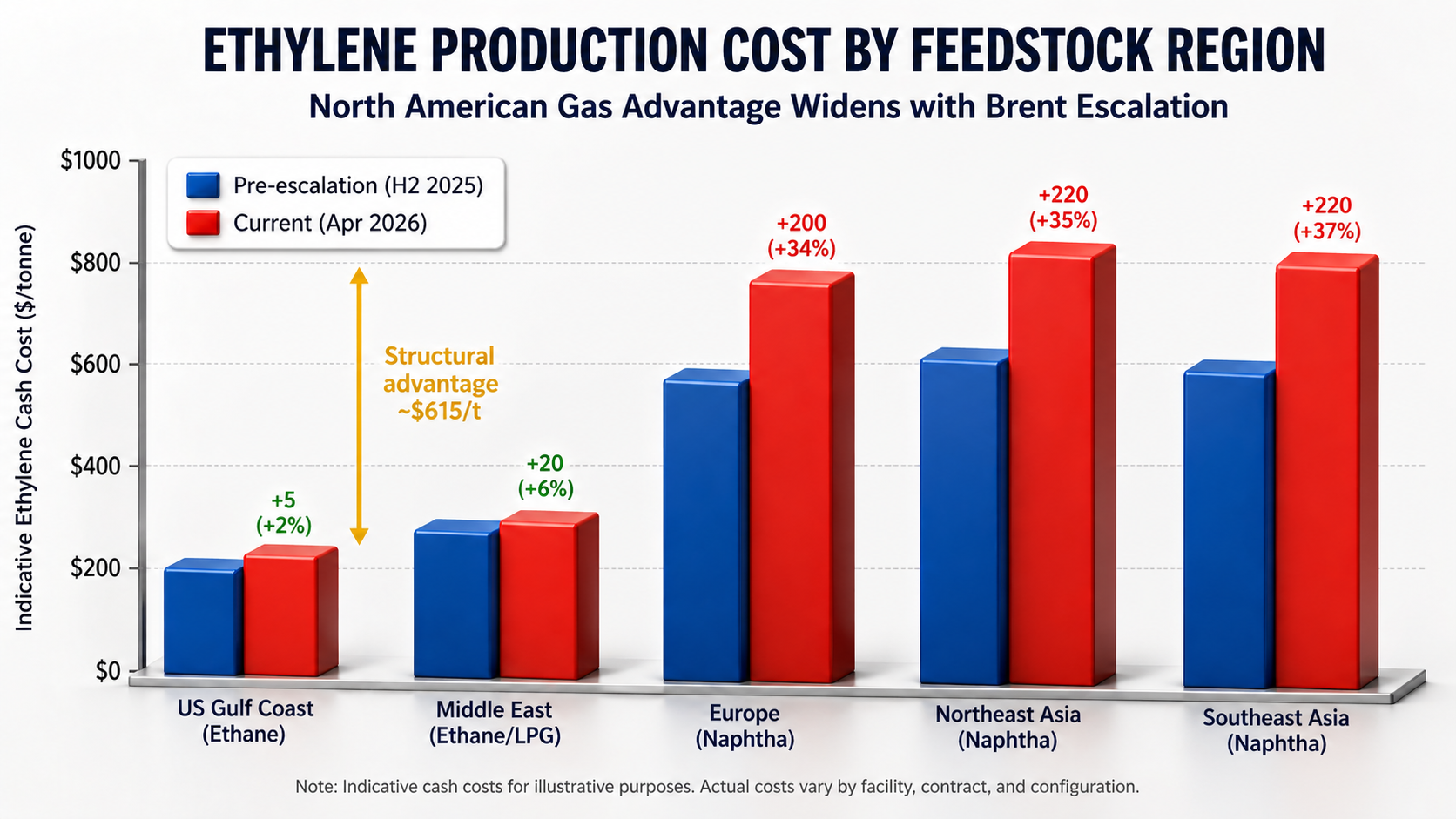

For downstream petrochemical producers, the implications of sustained Brent strength are direct and consequential. The critical variable is feedstock linkage: naphtha, the primary olefins feedstock for crackers in Asia and much of Europe, is priced as a derivative of crude. When Brent rises, naphtha rises. When naphtha rises, the cash cost of producing ethylene and propylene from liquid feedstocks rises with it — compressing margins in an already difficult operating environment.

North American producers, operating crackers predominantly fed by ethane derived from natural gas liquids, are structurally decoupled from this dynamic. US ethane prices have remained relatively stable, and the structural advantage that North American producers hold over their Asian and European counterparts — already significant in recent years — widens further as Brent-linked feedstock costs escalate.

Figure 4: Indicative ethylene cash costs by feedstock region. The North American ethane advantage widens materially as Brent-linked naphtha costs escalate.

“We have not seen feedstock cost divergence this pronounced since the early years of the US shale build-out. Asian crackers are being squeezed from both ends — naphtha costs rising with Brent while derivative pricing remains under pressure from overcapacity. The North American advantage is not temporary; current geopolitics are simply making it more visible, and more painful for those on the wrong side of it.”

— Senior analyst, Asia-Pacific petrochemicals research, global commodities consultancy

This is not a new structural trend. The shale revolution fundamentally altered the global feedstock cost curve, creating a persistent and substantial competitive advantage for US-based ethylene production. What the current geopolitical environment does is amplify and extend that advantage, with implications for trade flows, capacity utilisation decisions, and investment allocation across the global petrochemicals industry.

Asia & Europe: Naphtha crackers face rising feedstock costs as Brent strengthens, directly pressuring ethylene margins.

North America: US ethane-based producers retain a structural cost advantage that widens materially in periods of crude-linked feedstock inflation.

Middle East: LNG feedstock costs for gas crackers remain relatively insulated, though regional logistical risk introduces its own uncertainty.

Polypropylene: Producers reliant on propylene as a refinery co-product face additional pressure as refinery run rates respond to crude price signals.

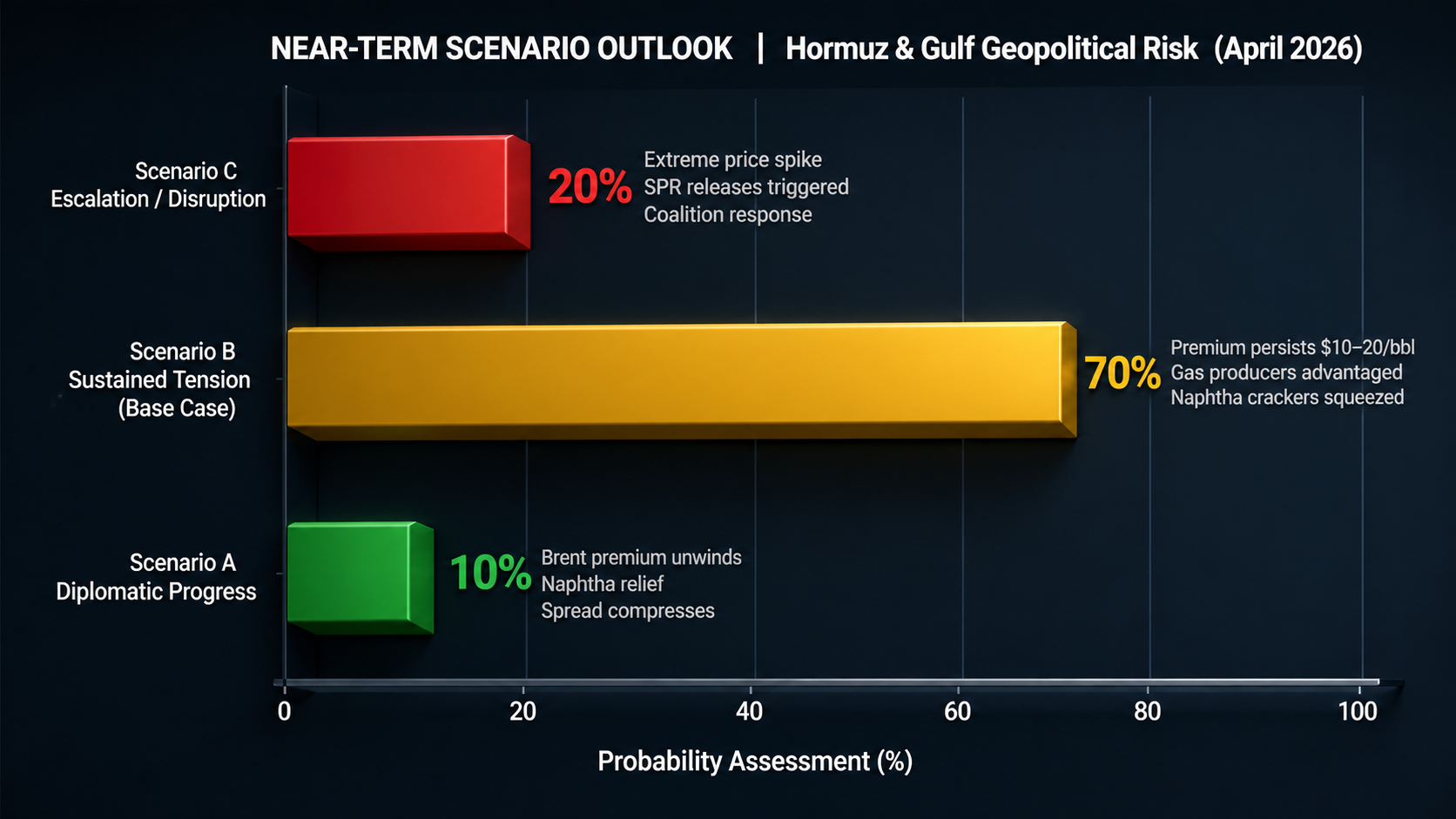

OUTLOOK: THREE SCENARIOS FOR MARKET PARTICIPANTS

The range of plausible near-term outcomes spans from contained tension to meaningful disruption. Market participants should be scenario-planning across at least three distinct paths:

Figure 5: Near-term scenario probability assessment for Hormuz and Gulf geopolitical risk, April 2026. Base case remains sustained tension without full escalation.

Scenario A — Diplomatic Progress (Low Probability Near-Term)

A verifiable de-escalation — whether through a framework agreement, confidence-building measures, or a negotiated reduction in regional military posture — would trigger a rapid unwinding of the geopolitical premium in Brent. Naphtha-linked producers would see immediate feedstock cost relief. The Brent-WTI spread would compress. This scenario requires genuine political will on multiple sides and is not the base case.

Scenario B — Sustained Tension, No Escalation (Base Case)

The most likely near-term path is a continuation of elevated but stable geopolitical risk. Diplomacy remains active without producing resolution. Naval postures are maintained. Hormuz remains open but expensive. The geopolitical premium persists in the $10–$20/bbl range, favouring gas-based producers and penalising naphtha-linked crackers. This is a manageable but structurally costly environment for Asian and European petrochemical operators.

Scenario C — Escalation and Partial Disruption (Tail Risk)

A significant escalation event — mining incidents, direct military engagement, or a declared naval exclusion zone — would trigger emergency policy responses from major consuming nations, extreme crude price spikes, and severe dislocation in petrochemical feedstock markets globally. Strategic reserve releases and coalition naval responses would follow rapidly, but the short-term damage to supply chains and pricing would be severe. This scenario is not base case, but its probability is non-trivial.

CONCLUSION

The Strait of Hormuz has always been important. What has changed is the market’s willingness to price that importance in real time rather than in retrospect. The geopolitical risk premium now embedded in Brent crude is not noise — it is a rational market response to a measurably more complex operating environment.

For energy markets, the central variable is now the gap between diplomatic signalling and operational reality. Until that gap closes — through verifiable de-escalation, not merely the appearance of engagement — Brent will retain its premium over landlocked benchmarks, naphtha-linked crackers will face structural cost pressure, and the competitive advantage of North American gas-based producers will continue to widen.

This is not a transient shock to be managed through short-term hedging alone. It is the energy market in the process of recalibrating its structural risk model — and that recalibration has implications that will play out across crude, LNG, and petrochemical markets for months, not days.

DISCLAIMER: This commentary is published for informational purposes only and does not constitute investment advice, a solicitation, or an offer to buy or sell any commodity or financial instrument. While every effort has been made to ensure accuracy, Polymerupdate makes no representations as to the completeness or reliability of the information herein. All market data and price references are indicative and subject to change. © 2026 Polymerupdate. All rights reserved. |