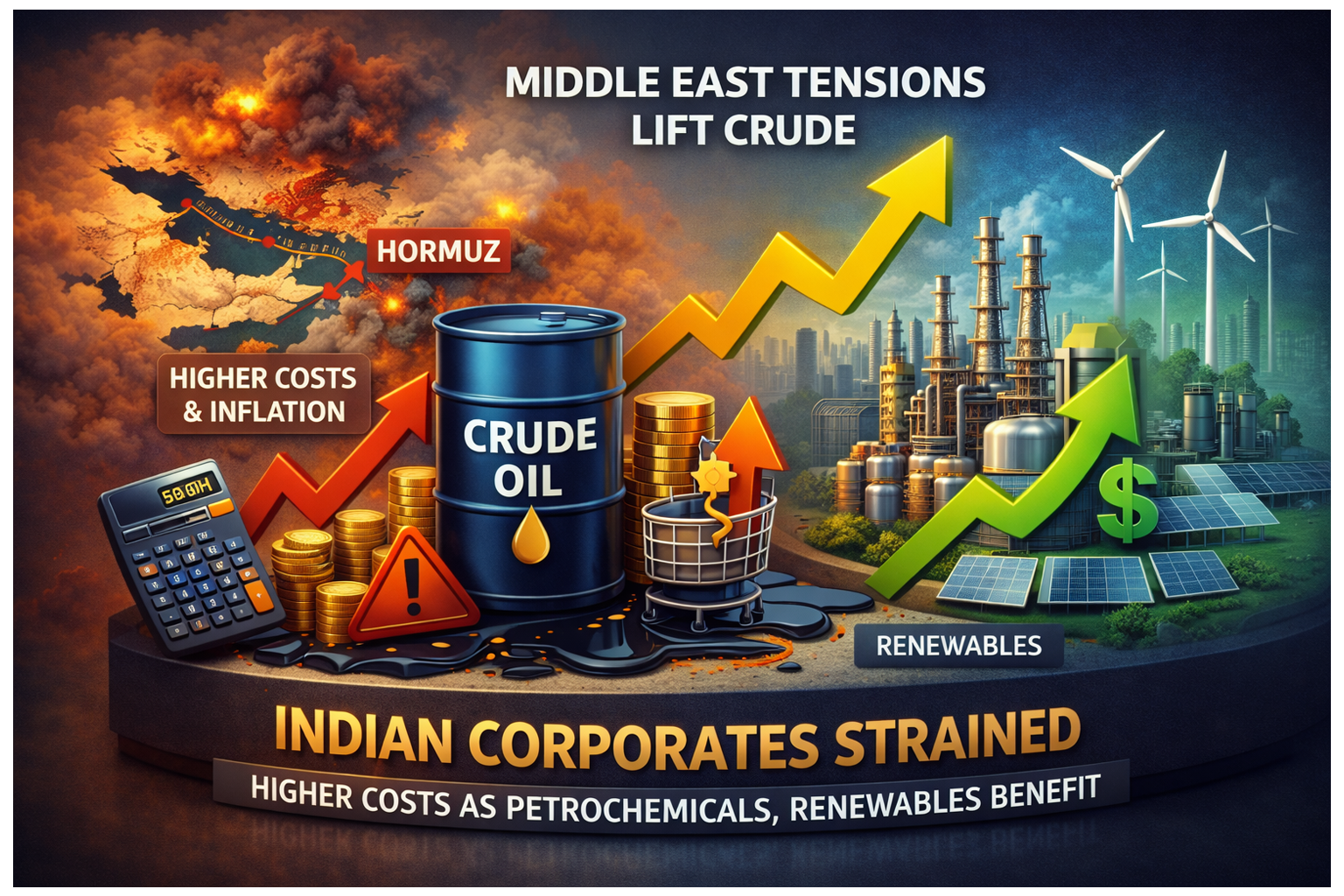

The Middle East conflicts could trigger a wide spectrum of impacts on Indian corporates, ranging from logistics bottlenecks and fuel shortages to inflationary pressures and capital reallocation. The immediate fallout is cost-driven, with sectors such as logistics, chemicals, fertilizers, cement, ceramics, city gas distribution (CGD), and oil marketing companies (OMCs) at risk. Consequently, these sectors could have a cascading effect on the Indian economy, India Ratings and Research said in its latest assessment of the impact of the Middle East crisis on India.

However, petrochemicals may benefit in the near term, while the renewable energy sector could gain in the medium to long term due to a greater emphasis on ensuring domestic energy security. The immediate credit impact is likely to be felt by entities in select categories, with higher-rated companies having sufficient buffers to manage short- to medium-term disruptions, the rating agency said in its latest report. Crude oil prices remain highly elevated, currently trading at around US$ 108 a barrel—about 50 percent higher than the pre-Israel–US–Iran conflict level of US$ 72 a barrel on February 27. The sharp rise in crude oil prices is likely to exert pressure on the current account deficit and the currency through imported inflation.

India’s swift actionsThe Union government has announced swift measures to help Indian corporates deal with the ongoing West Asia crisis, which has escalated following joint missile and drone strikes by Israel and the US on Iran, and Tehran’s retaliation targeting US military installations and civilian infrastructure in Gulf countries, along with direct strikes on Tel Aviv. On Friday, India announced a reduction in excise duty on petroleum products, with the special additional excise duty (SAED) on petrol cut from Rs 13 per litre to Rs 3 per litre.

In the case of diesel, SAED has been reduced to nil from Rs 10 per litre. These duty cuts have been offset by the imposition of export duties on diesel at Rs 21.50 per litre and on aviation turbine fuel (ATF) at Rs 29.5 per litre. The objective is to ensure adequate availability of these fuels in the domestic market. The benefit of these reductions will accrue to oil marketing companies (OMCs), which have been bearing higher costs, with under-recoveries rising as crude oil prices have increased by over 50 percent since the war began. There will be no change in the retail prices of petrol or diesel.

“There will certainly be periodic reviews of the pricing situation in relation to costs. However, if the current matrix remains unchanged, the total loss of revenue for the government could be in the range of Rs 1.3–1.4 lakh crore (assuming a Rs 10 reduction on a permanent basis for the entire year with no change in consumption). This would need to be offset through expenditure cuts in other areas to maintain fiscal balance. In an extreme scenario where there is no change in revenue or expenditure—i.e., ceteris paribus (holding other factors constant)—the fiscal deficit could come under upward pressure of around 0.4 percent of GDP. This could be one reason why bond yields hardened significantly today by over 10 basis points (bps),” commented Madan Sabnavis, Chief Economist, Bank of Baroda.

India’s GDP growth projectionsConsidering ongoing developments, global financial services company S&P, in its latest quarterly Asia-Pacific economic commentary, has raised India’s gross domestic product (GDP) growth forecast by 0.4 percentage points to 7.6 percent for the financial year 2025–26 and to 7.1 percent for the financial year 2026–27. The rating agency cited strong domestic demand drivers such as private consumption, investment, and steady exports as the primary engines of growth. However, it cautioned that ongoing Middle East tensions could strain the fiscal position due to higher energy prices arising from the conflict.

The Organisation for Economic Co-operation and Development (OECD) has also forecast that the Indian economy will expand by 7.6 percent in the financial year 2025–26, before moderating to 6.1 percent the following year and 6.4 percent in the financial year 2027–28. The organisation noted that the evolving conflict in the Middle East has “human and economic costs” for countries directly involved and could test the resilience of the global economy by disrupting energy supplies and raising commodity prices.

The multilateral body projected that a closure of the Strait of Hormuz and the resultant high energy prices could push retail inflation from 2 percent in the financial year 2025–26 to 5.1 percent in 2026–27, before easing to 4.1 percent in the subsequent financial year. It also warned that risks stemming from renewed geopolitical tensions and persistent trade-related uncertainties could impact India through fluctuations in commodity prices, trade volumes, and capital flows.

Intensifying macroeconomic pressuresCost escalation in the logistics sector is inevitable, as it is the first to absorb the shock. With the Strait of Hormuz nearly inactive, only selective cargoes are receiving clearance. Most Middle Eastern ports remain technically open but are witnessing negligible vessel movement, with Jeddah and King Abdullah acting as the only meaningful operational gateways. Freight charges have surged due to emergency rate levies, bunker surcharges, and newly introduced air freight fuel surcharges. Meanwhile, some global carriers are offering hybrid models—i.e., de-boarding cargo at safer ports followed by inland movement—to maintain supply chains. Certain Indian container-handling companies have also announced temporary relief measures.

After a weak cycle through 2025, profitability in the petrochemical sector is expected to surge in March, with spreads widening sharply and companies booking inventory gains. Close to 20 percent of full-year profitability may accrue in just the March quarter. In the city gas distribution (CGD) segment, compressed natural gas (CNG) and domestic piped natural gas (PNG) have been protected from allocation cuts, but industrial and commercial consumers face steep reductions in gas availability. CGD entities with strong balance sheets and credit profiles are likely to remain resilient. Sectors such as tiles and glass—dependent on continuous furnaces—are already under stress, as reflected in recent rating actions.

For oil marketing companies (OMCs), while diesel cracks have remained strong, marketing margins are constrained as retail prices have not been fully revised. Elevated crude prices could reintroduce under-recoveries if the price freeze continues. However, these entities are likely to benefit from government support and maintain their credit profiles.

Chemicals and petrochemicalsCommodity chemical producers with index-linked pricing are passing on cost increases more effectively than specialty players, who face greater negotiation hurdles and limited pricing power. Scarcity of raw materials such as methanol, ethylene, propylene, butadiene, naphtha, and helium is pushing several manufacturers toward partial shutdowns, a situation that could worsen if the conflict persists. The sector has already been challenged by excess supply from China and could face further credit stress if the situation prolongs.

The fertiliser industry is acutely exposed, as gas serves both as a feedstock and a fuel. If the allocation of industrial gas becomes more constrained, companies may be forced to rely on inventories, undertake advance maintenance shutdowns, or divert limited gas to priority units. Prolonged shortages could necessitate higher imports and escalate subsidy requirements—potentially by Rs 500–600 billion.

The renewable energy sector could be among the few beneficiaries of the energy crisis over the long term, as India places greater emphasis on domestic energy security amid rising geopolitical risks. High liquefied natural gas prices (with spot prices around US$22/mmBtu) make green hydrogen more attractive, with production costs of US$4–4.5/kg. As industries shift toward electrified alternatives and diversify energy sources, renewable capacity—particularly solar—may gain momentum. Green hydrogen plants themselves are heavily solar-linked, creating a multiplier effect across the renewable ecosystem.

DILIP KUMAR JHA

Editor

dilip.jha@polymerupdate.com