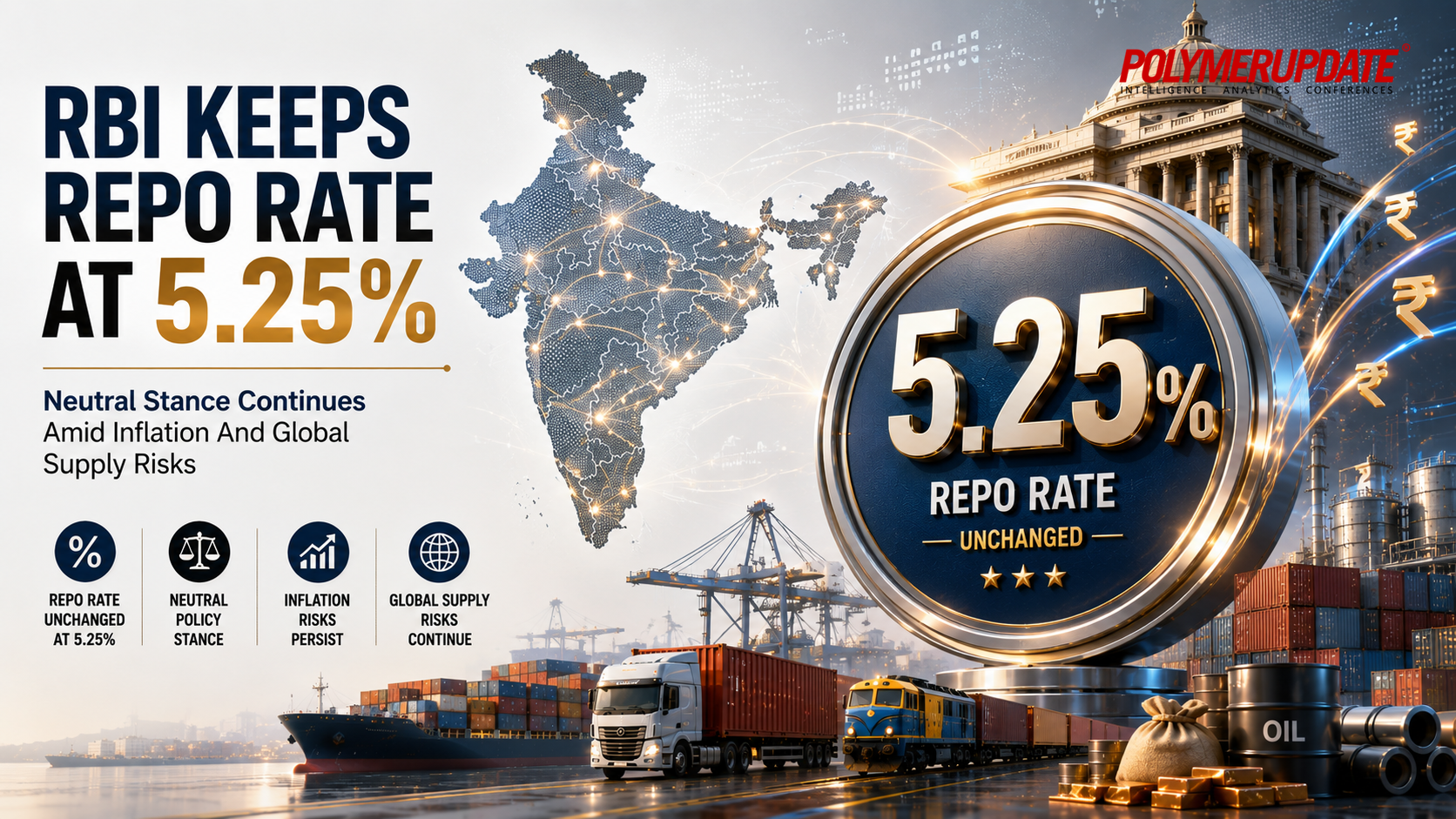

The Reserve Bank of India (RBI) on Friday kept the repo rate unchanged at 5.25 percent due to a sudden increase in pressure on the Indian economy following widening geopolitical conflicts in the Middle East, with hopes of respite remaining dim despite optimism. With this, the repo rate under the liquidity adjustment facility (LAF) remained unchanged at 5.25 percent. Consequently, the standing deposit facility (SDF) rate continued at 5 percent, while the marginal standing facility (MSF) rate and the Bank Rate remained at 5.5 percent. The Monetary Policy Committee (MPC) also decided to continue with the neutral stance.

The decision was taken unanimously after the Monetary Policy Committee (MPC) deliberated for three days from June 3 to 5 and assessed the evolving macroeconomic and financial developments, along with the outlook. The committee noted that the global environment has deteriorated since the last policy meeting, with the conflict lingering amid a fragile truce. The adverse implications of extended supply chain disruptions and elevated energy prices are reflected in the moderation in growth and the increase in inflation projections from the April policy.

Sanjay Malhotra, Governor of the RBI, stated, “The global economy has been shaped by heightened uncertainty over the past few months, disruptions to key trade routes and supply chains, increased market volatility, and cautious business sentiment. I must emphasise that the Indian economy entered this episode of global turbulence with much better fundamentals than in previous similar episodes. While we remain confident of withstanding these shocks with minimal pain, it is important not only to confront and address these challenges but also to treat them as an opportunity to further enhance resilience.”

He further added, “The global economic outlook remains clouded by the continuing geopolitical impasse in West Asia, as sharply escalating energy prices and global supply chain disruptions continue to hinder economic activity. Faced with difficult trade-offs, monetary policy has turned more cautious. Major advanced economy central banks are likely to pivot towards monetary policy tightening. While equity markets remain buoyant, driven by AI-fuelled optimism, global bond markets remain bearish amid renewed inflation fears and continuing debt sustainability concerns. Risk-off sentiment and safe-haven demand are imparting volatility to forex markets, with a depreciating trend visible in many EME currencies.”

Observations

ObservationsIndia’s retail inflation remains below the target despite global shock as the pass-through to domestic prices has been limited. While the baseline projections point towards headline inflation firming up towards the upper tolerance level in the October-December 2026 quarter, the impact of the supply shock is expected to wane January-March 20227 quarter onwards. The underlying inflation pressures continue to remain benign at this juncture. However, generalisation of inflation through second-round effects on expectations and wages is a distinct possibility, warranting a close vigil. The outlook also remains clouded due to the sub-normal south-west monsoon forecast and El Niño risks.

As for growth, elevated energy prices coupled with global supply constraints are having adverse spillovers on economic activity. While domestic demand remains resilient and manufacturing and services sectors activity continue to expand, there are incipient signs of moderation in some sectors as suggested by high frequency indicators. Further, there are considerable risks to the baseline assessment of inflation and growth due to the uncertainty about the duration and intensity of the conflict, magnitude of its spillover effects and the pace of restoration of supply chains.

Additionally, the food outlook remains uncertain on account of the sub-normal south-west monsoon forecast and El Niño. Although risks of higher inflation have amplified, the MPC felt it would be prudent to wait for greater clarity to emerge. Accordingly, the MPC voted to keep the policy rate unchanged. At the same time, the MPC will continue to remain data-dependent and closely monitor the developments, including supply side pressures getting embedded in the general price level and inflation expectations. The MPC also decided to retain the neutral stance.

GDPThe Second Advance Estimates released by the National Statistical Office (NSO) placed India’s real GDP growth at 7.6 percent in 2025-26, owing to strong expansion in private consumption and fixed investment. Robust performance of manufacturing and services sectors were the growth drivers from the supply side. As per several high frequency indicators, domestic economic activity remained largely steady since the outbreak of the conflict.

India’s manufacturing and services PMI suggest that both sectors continue to be resilient, and business expectations are still positive. On the demand side, private consumption, aided by discretionary spending, has remained resilient so far. Fixed investment has also maintained its momentum despite cost pressures. Merchandise exports recorded strong growth in April 2026, notwithstanding elevated freight and insurance costs. Services exports are also holding up well, reflecting sustained demand despite concerns about AI. Overall, the economic situation has broadly exhibited resilience and withstood the conflict spillovers, although the impact of cost pressures is becoming visible.

Going ahead, the rise in prices of energy and other inputs, coupled with supply disruptions, is likely to weigh on economic activity. Considering all potential developments, RBI projected India’s gross domestic product (GDP) growth at 6.6 percent for the full financial year 2026-27, with April-June quarter or Q1 at 6.6 percent; July-September quarter or Q2 at 6.3 percent; October-December quarter or Q3 at 6.5 percent; and January-March 2027 quarter or Q4 at 6.8 percent. The central bank cautioned that prolonged global supply chain disruptions, volatility in global financial markets, and weather-related shocks continue to pose downside risks to the domestic growth outlook.

Retail inflationAlthough firming up marginally from 3.2 percent in February, headline CPI inflation was below the target during March and April 2026 (3.4 percent and 3.5 percent, respectively). While food inflation edged up, fuel inflation remained muted as retail prices of petrol and diesel were unchanged in March and April. Core inflation remained stable at 3.7 percent during March-April. Excluding precious metals, core inflation was much lower at 2.1-2.2 percent during the same period. International crude oil prices (Indian basket) have averaged around US$ 110 a barrel during April-May 2026 and indications are that average oil prices for 2026-27 would be substantially higher than what were assumed during the last policy statement. Higher energy prices and an increase in several input prices also led to a sharp spike in WPI inflation in April 2026.

Turning to the inflation outlook, the partial pass-through of high global crude oil prices to domestic pump prices of petrol and diesel started since May. Prices of several inputs such as commercial LPG, industrial raw materials, chemicals, base metals, rubber, and plastic products, among others, have increased. These could exert upward pressure on CPI inflation in the coming months as firms pass on higher input costs. Given all prevailing fundamentals, the central bank projects India’s CPI inflation for 2026-27 at 5.1 percent with Q1 at 4.2 percent; Q2 at 5.1 percent; Q3 at 5.9 percent; and Q4 at 5.4 percent. Core inflation is projected at 4.7 percent for 2026-27.

External shocksOn the external financing front, buoyant gross foreign direct investment (FDI) and higher net FDI in 2025-26 underscore the continued interest of global investors in India. The FDI flows have also been encouraging in April 2026. During 2026-27 so far (till June 2), net FPI to India, however, witnessed outflows of US$ 13.7 billion, primarily in the equity segment.

RBI further unveiled that as on May 29, 2026, India’s foreign exchange reserves stood at a healthy US$ 682.3 billion, adequate in terms of the standard metrics of reserve adequacy including import cover (about 11 months) and external debt (89.1 percent). Various policy initiatives are expected to strengthen our balance of payments. These include the recent agreements with major trading partners, opening the insurance sector to 100 percent FDI, ethanol blending program, push for energy transition, easing of FDI restrictions for land-bordering countries, liberalisation of the ECB framework, and several others.

DILIP KUMAR JHA

Editor

dilip.jha@polymerupdate.com